How I Finally Took Control of My Money — A Beginner’s Journey to Real Financial Freedom

I used to think financial freedom was just for people with high salaries or lucky breaks. But after years of living paycheck to paycheck, I realized it wasn’t about how much I earned — it was about what I did with it. I made mistakes, fell into traps, and ignored my finances until stress took over. Then I started small: tracking spending, building a safety net, and learning how money really works. This is my story — not as an expert, but as someone who finally got serious about wealth management. If I can do it, so can you.

The Wake-Up Call: When Money Stress Became Too Loud to Ignore

There was a moment — not dramatic, not cinematic — when I sat at my kitchen table, staring at a stack of unpaid bills, and realized I could no longer pretend everything was fine. My car had broken down the week before, and the repair cost more than I had in my checking account. I used a credit card, telling myself it was a one-time emergency. But deep down, I knew it wasn’t the first time, nor would it be the last. That month, I spent more than I earned, again. The pattern was clear: income came in, disappeared without explanation, and left me anxious every time a new expense appeared. The stress wasn’t just about money — it was about feeling powerless. I couldn’t plan for a vacation, help my family, or even sleep well at night.

Like many people, I carried beliefs that kept me stuck. I told myself, “I don’t earn enough to save,” or “Investing is for people who already have money.” These thoughts felt true at the time, but they were excuses disguised as facts. The truth is, financial struggle isn’t always about income — it’s about habits, awareness, and control. I began to see that my real problem wasn’t a lack of money, but a lack of attention. I was managing my household, my time, and my responsibilities with care, yet I treated my finances like an afterthought. That disconnect was costing me more than dollars — it was costing me peace of mind.

The turning point came when I admitted I didn’t need a raise to change my situation — I needed a mindset shift. I stopped blaming my paycheck and started asking better questions: Where is my money going? What can I control? What small step can I take today? That shift — from helplessness to agency — was the foundation of everything that followed. I didn’t have all the answers, but I was finally ready to look for them. And the first step was simply paying attention.

Building the Foundation: Managing Cash Flow Like a Pro (Without the Jargon)

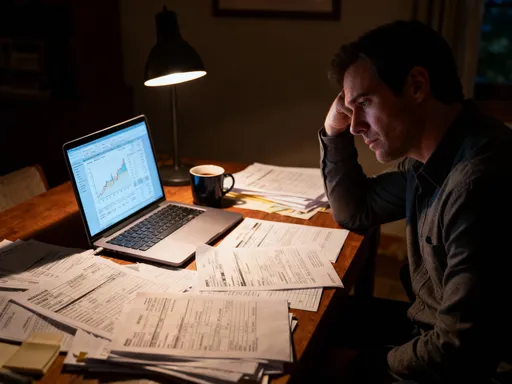

Once I decided to take control, the next question was where to start. I didn’t have a finance degree or a stockbroker on speed dial. What I did have was a notebook, a pen, and a willingness to be honest. I began tracking every dollar that came in and went out — not with a complicated app, but with a simple spreadsheet I made in a free online tool. At first, it felt tedious. But within two weeks, patterns emerged that surprised me. I saw how much I spent on subscription services I barely used, how often I grabbed takeout when I was tired, and how little I was setting aside for savings. The numbers didn’t lie — and they gave me power.

I learned to separate my spending into two categories: fixed and variable. Fixed expenses — like rent, utilities, and insurance — were predictable and necessary. Variable expenses — like groceries, dining out, and shopping — were where I had real control. By focusing on the variable side, I found opportunities to adjust without sacrificing comfort. I didn’t cut everything — I just became intentional. For example, I switched to a cheaper phone plan, cooked more meals at home, and set a monthly limit for non-essential purchases. These weren’t drastic changes, but they added up.

The most powerful tool I discovered was budgeting — not as a restrictive rulebook, but as a financial roadmap. I created a simple plan that matched my income and priorities. I paid myself first by scheduling automatic transfers to a savings account every time I got paid. This ensured that saving wasn’t an afterthought — it was a priority. I also built in flexibility, allowing room for occasional treats so I wouldn’t feel deprived. Over time, this system became second nature. I wasn’t perfect — there were months when I overspent — but I learned to adjust and keep going. Consistency, not perfection, became my goal.

What I realized is that managing cash flow isn’t about being rich — it’s about being aware. You don’t need a high salary to build a strong financial foundation. You need clarity, discipline, and a plan. By taking control of my daily money habits, I stopped feeling like a passenger and started feeling like the driver. And that shift made everything else possible.

Safety First: Why Risk Control Is More Important Than Big Wins

Early on, I thought the key to financial freedom was making money — getting a bonus, earning interest, or hitting a lucky investment. But I soon learned that protecting what I already had was far more important. Wealth isn’t built by chasing returns — it’s preserved by managing risk. The real danger wasn’t missing out on gains — it was losing what I had worked so hard to save. That’s why my next focus became risk control: creating buffers that could protect me when life threw unexpected challenges my way.

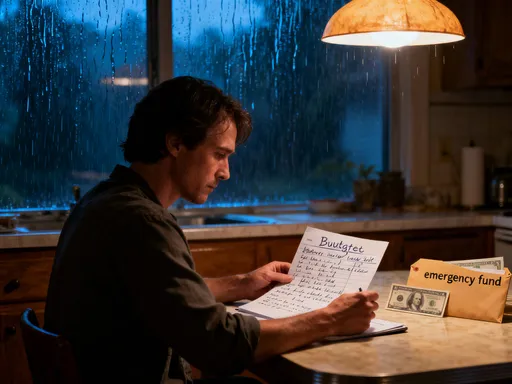

The first step was building an emergency fund. I started small — just $20 a week — and kept it in a separate savings account. The goal wasn’t to get rich, but to avoid panic when emergencies happened. When my washing machine broke, I paid for repairs without touching my credit card. When a medical bill arrived, I had the cash to cover it. That fund became my financial shock absorber. Experts often recommend three to six months of living expenses, but I learned that even a small cushion makes a big difference. It’s not about the amount — it’s about the confidence it brings.

I also took a hard look at debt. High-interest credit card balances were draining my budget and keeping me stuck. I used the snowball method — paying off the smallest balance first while making minimum payments on others — because it gave me quick wins and kept me motivated. As each card was paid off, I redirected that payment toward the next one. It took time, but the progress was real. I also avoided lifestyle inflation — the habit of spending more as income rises. When I got a small raise, I didn’t upgrade my car or move to a bigger apartment. Instead, I increased my savings rate. That discipline protected me from the trap of always living at the edge of my income.

Another key part of risk control was insurance. I reviewed my health, auto, and renters policies to make sure I had adequate coverage without overpaying. I learned that insurance isn’t an expense — it’s a safeguard. It doesn’t make you richer, but it prevents you from becoming poorer overnight. Together, these steps — saving, reducing debt, and protecting against risk — created a foundation of stability. That stability didn’t feel exciting, but it was empowering. It meant I could face the future with confidence, not fear.

Growing Wealth Without Gambling: My First Steps Into Smart Investing

Once I had control over my cash flow and a safety net in place, I was ready to think about growing my money. But the idea of investing scared me. I’d heard stories of people losing everything in the stock market, or getting rich overnight from risky bets. I didn’t want to gamble — I wanted to grow. So I focused on learning the basics: diversification, low-cost funds, and compound growth. I realized that successful investing isn’t about picking the next big stock — it’s about patience, consistency, and staying the course.

I started with index funds — simple, low-cost investments that track the overall market. Instead of trying to beat the market, I decided to ride it. I opened a retirement account and began contributing a small amount each month. I chose funds with low expense ratios because I knew fees eat into returns over time. At first, the growth was slow. My account balance didn’t double overnight. But I kept adding money, and over time, I saw the power of compound interest — earning returns not just on my contributions, but on the returns themselves. It was like planting a tree: I wouldn’t see shade for years, but I knew it would grow if I kept watering it.

I also learned to ignore the noise. The financial news was full of predictions, hot tips, and market panic. But I stayed focused on my long-term goals. I didn’t try to time the market or chase trends. I rebalanced my portfolio once a year to keep my risk level in check. And I avoided emotional decisions — like selling during a downturn — because I knew that time in the market matters more than timing the market. My strategy wasn’t exciting, but it was effective. I wasn’t trying to get rich quickly — I was building wealth slowly and steadily.

One of the biggest lessons was that investing isn’t just about money — it’s about mindset. It taught me to think long-term, to delay gratification, and to trust the process. I didn’t need to be a genius or take big risks. I just needed to be consistent. And by starting small and staying disciplined, I began to see my money work for me — not the other way around.

The Habits That Stick: Turning Good Moves Into Lasting Change

Knowledge is powerful, but habits are what create real change. I could read all the finance books in the world, but if I didn’t act consistently, nothing would improve. So I focused on building routines that supported my goals. The most effective one was automation. I set up automatic transfers to my savings and investment accounts the day after I got paid. That way, I never had to decide whether to save — it just happened. I also scheduled monthly check-ins with my budget, reviewing my spending and adjusting as needed. These small rituals kept me on track without requiring constant willpower.

I also learned to connect my financial goals to deeper values. Saving wasn’t just about numbers — it was about security, freedom, and peace of mind. I imagined a future where I could handle emergencies without stress, take a family trip without guilt, or retire with dignity. Those visions kept me motivated when old habits tempted me to overspend. I celebrated small wins — paying off a credit card, reaching a savings milestone — not with shopping, but with experiences like a nice dinner or a day outdoors. That reinforced the idea that financial discipline leads to real rewards.

Of course, setbacks happened. There were months when unexpected expenses disrupted my budget, or when I felt discouraged by slow progress. But I learned to treat those moments with compassion, not criticism. I didn’t quit — I adjusted. I reminded myself that financial health, like physical health, is a journey. It’s not about being perfect — it’s about showing up consistently. Over time, these habits became part of my identity. I wasn’t just someone who saved money — I was someone who valued financial responsibility.

What I discovered is that lasting change doesn’t come from big leaps — it comes from small, repeated actions. The power isn’t in one decision, but in the pattern. By making smart choices a normal part of my life, I built momentum that carried me forward, even on the hard days.

Avoiding the Traps: Lessons from My Biggest Money Mistakes

No financial journey is perfect — mine certainly wasn’t. I made mistakes, and some of them were costly. One of the biggest was emotional spending. After a tough day at work or a personal setback, I’d go online and buy something — clothes, gadgets, home decor — to feel better. It gave me a temporary high, but the regret lasted much longer. I learned that money can’t fix emotions, and shopping isn’t therapy. Now, I have a 24-hour rule: if I want to make a non-essential purchase, I wait a day. Most of the time, the urge passes.

Another mistake was chasing trends. I once invested in a “hot” stock because everyone was talking about it. I didn’t understand the business — I just wanted to be part of the excitement. When the price dropped, I panicked and sold at a loss. That experience taught me to do my own research and avoid herd mentality. Now, I question every financial decision: What’s the risk? What’s the fee? Does this align with my goals? I also learned to be skeptical of “get-rich-quick” schemes — whether it’s crypto hype, multi-level marketing, or too-good-to-be-true returns. If something sounds unrealistic, it probably is.

I also ignored fees for too long. I didn’t realize how much I was paying in bank charges, investment fees, and subscription renewals. Over time, those small costs added up to hundreds of dollars a year. Now, I review all my accounts regularly and look for ways to reduce expenses. I switched to low-fee investment options, canceled unused services, and negotiated better rates when possible. These changes didn’t require big sacrifices — just attention.

Looking back, I’m grateful for my mistakes — not because they were good, but because they taught me. They showed me where I was vulnerable and helped me build stronger defenses. By sharing them, I hope others can avoid the same pitfalls and move forward with greater awareness.

Freedom in Motion: What Financial Control Actually Feels Like

Today, financial freedom doesn’t mean I’m rich. It means I’m in control. I still budget, I still save, and I still plan. But the stress is gone. I no longer wake up worried about bills or feel anxious when the phone rings. I can make choices based on what matters to me — not what my bank account forces me to do. I’ve taken family trips, helped loved ones in need, and started thinking seriously about retirement. These aren’t luxuries — they’re the result of consistent, thoughtful money management.

What surprised me most was how much peace of mind matters. The emotional weight of financial stress is heavy — it affects sleep, relationships, and self-worth. Letting go of that burden has improved my life in ways I didn’t expect. I feel calmer, more confident, and more capable. I’ve learned that wealth isn’t just about numbers — it’s about freedom, security, and the ability to live with intention.

This journey didn’t happen overnight. It took years of small decisions, occasional setbacks, and continuous learning. But every step was worth it. I didn’t need a miracle — I just needed to start. And the truth is, anyone can do this. You don’t need a high income, a finance degree, or perfect discipline. You need awareness, a plan, and the courage to begin. Financial freedom isn’t a destination — it’s a practice. It’s not about having everything — it’s about knowing you’ll be okay, no matter what comes next. And that, more than any dollar amount, is the real definition of wealth.